Will Your Institution Pass It's FIC Act Audit?

Find Out With A Quick Free FICA Compliance Quiz.

Every Accountable Institution is obligated to comply with the Financial Intelligence Centre Act, 38 of 2001 (FIC Act). Find out in 2 minutes if your firm is vulnerable to financial crime abuse or at risk of FIC penalties and reputational damage.

No cost. No obligation. Instant results.

Who Are Accountable Institutions?

Many firms don’t realise they fall under the FIC Act until it’s too late.

If your business handles client funds, high-value goods, or large cash transactions, you’re likely required by law to have proper anti-financial crime compliance measures in place.

Law Firms & Attorneys

Property Practitioners & Estate Agents

Financial Service Providers & Advisors

High-Value Goods Dealers who sell a single item for R100 000 or more

Credit Providers who are subject to the National Credit Act (NCA)

Trust and Company Service Providers

Crypto Asset Service Providers

Value Transfer Provider

What Some of Our Clients Say:

Testimonials from law firm directors who have successfully navigated compliance implementation:

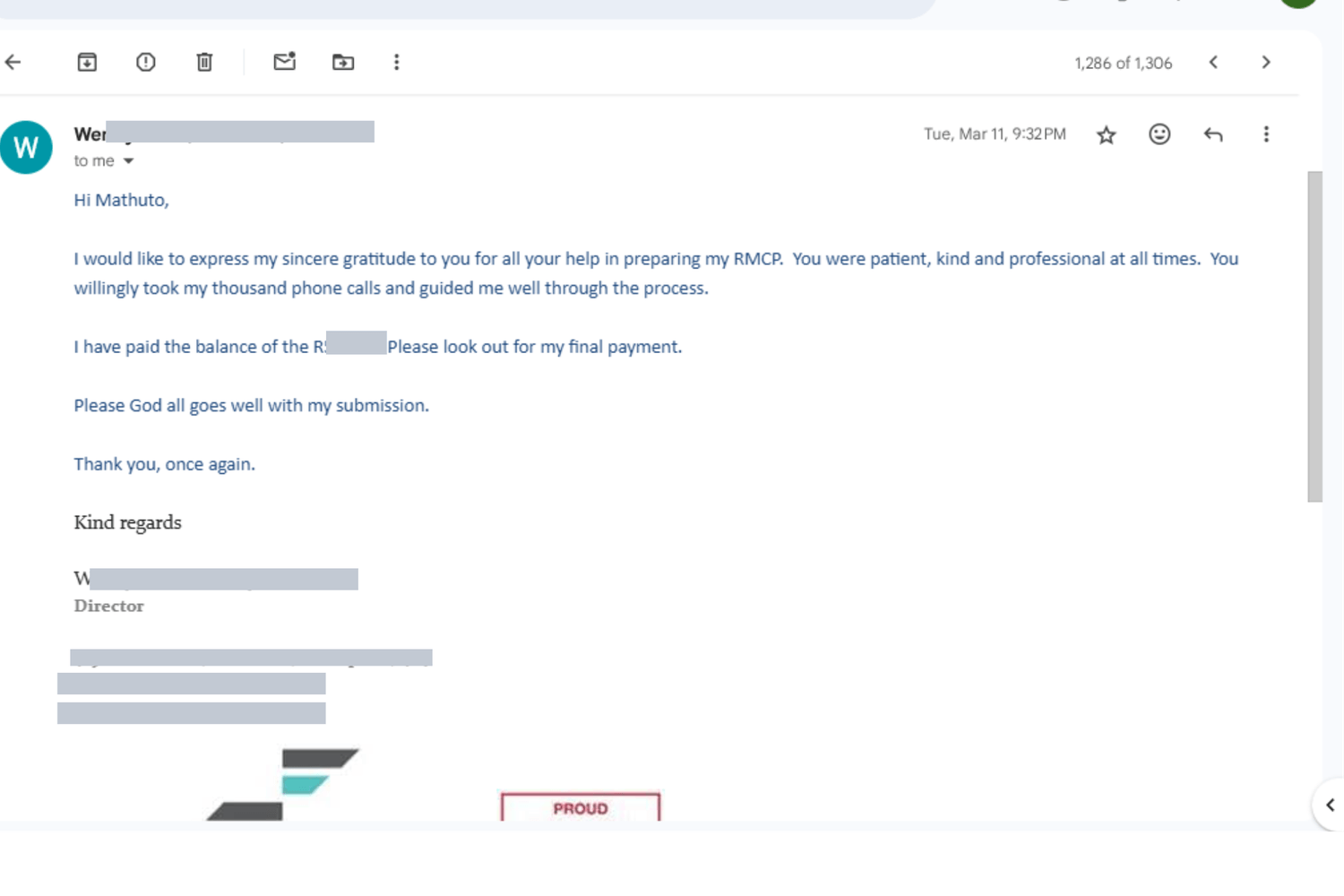

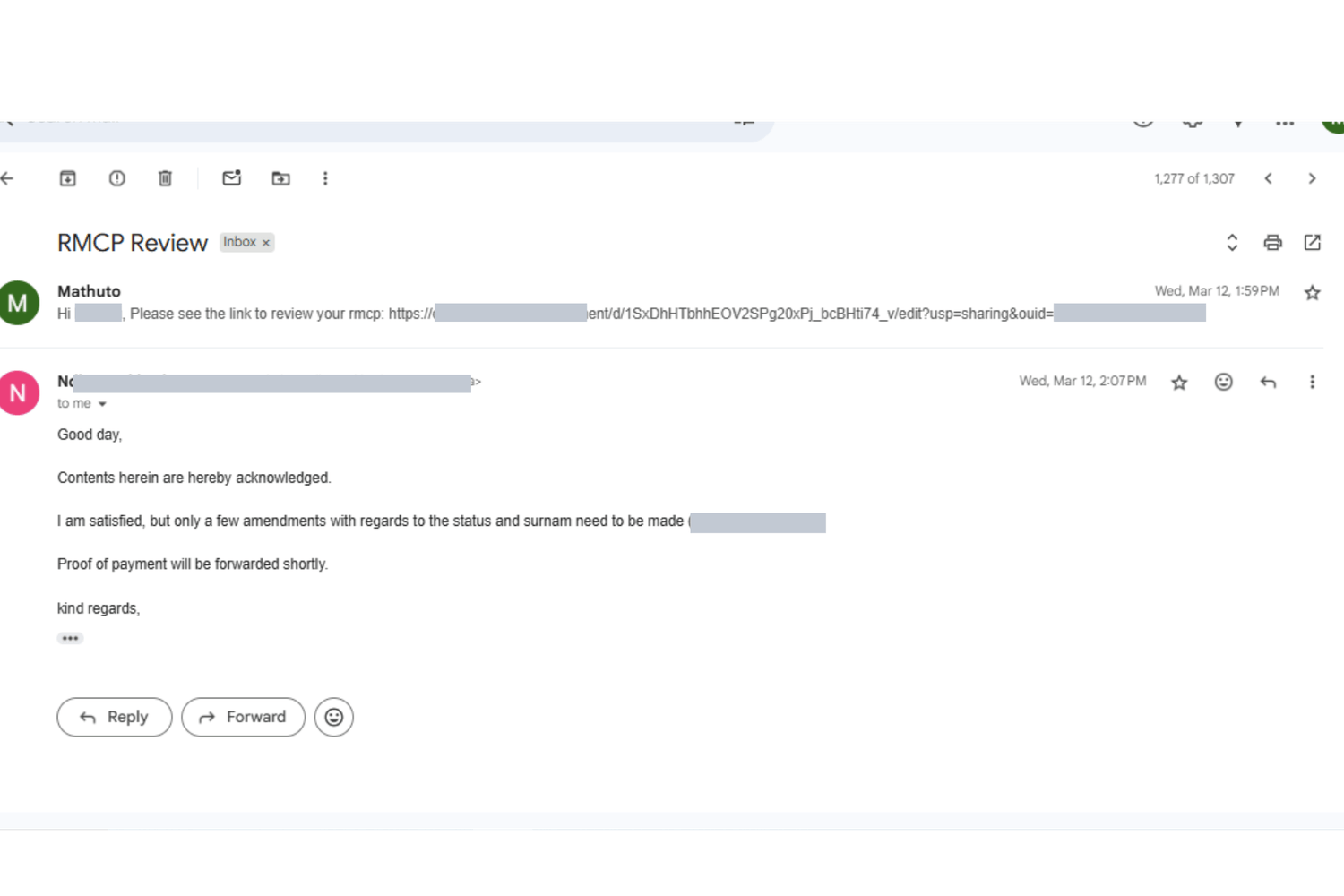

"From the initial audit to RMCP setup and staff training, FICA Friendly made compliance manageable and stress-free. We now operate confidently knowing we’re fully compliant."

— Director, EMG Attorneys Inc.

“FICA Friendly went above and beyond for my firm. They completely revamped my RMCP, guided me step by step, and gave me peace of mind during a stressful compliance process.”

— Director, MS Seconna Attorneys Inc.

— Director, SF Inc.

— Director, Ndlovu M. Attorneys Inc.

Let's Start Here: What are Your Financial Intelligence Centre Act Obligations as an Accountable Institution?

Watch this official explanation from the Financial Intelligence Centre regarding regulatory expectations and business impact:

The Financial Intelligence Centre Act (FIC Act) exists to protect South Africa’s financial system from abuse — including money laundering, terrorist financing, and other financial crimes.

If your business handles money, high-value goods, or large cash transactions, the law may require you to follow strict compliance steps.

Here’s what the FIC expects from accountable institutions:

Registering with the FIC.

Filing required regulatory reports.

Developing a Risk Management and Compliance Program (RMCP).

Conducting risk-based customer due diligence.

Establishing beneficial ownership of clients.

Checking clients against the targeted financial sanctions list.

Why this matters: Following these steps not only keeps regulators satisfied, it also protects your reputation, builds client trust, and strengthens South Africa’s financial system.

Accountable Institutions That Were Caught Off Guard

The penalties below demonstrate the FIC's systematic approach to enforcement across all Accountable Institution categories. These sanctions reflect the regulator's commitment to comprehensive compliance, regardless of institution size or perceived sophistication.

R 7.7 M

Fine

Kunene Ramapala Inc.

No Risk Management & Compliance Programme (RMCP)

Failed to screen clients against sanctions list

Improper goAML system management

Appeal rejected by FIC Appeal Board for "gross negligence and wilful disregard".

R 3 M

Fine

Ninety One Fund Managers

Deficient Risk Management & Compliance Programme

Inadequate client identification and verification

Failed ongoing due diligence requirements

R500,000 suspended for 3 years conditional on sustained compliance.

R 10 M

Fine

ABSA Bank

Failed customer due diligence on Politicallly Exposed Persons and FPPOs

Delayed transaction monitoring (8,559 alerts)

Missed 48-hour and 15-day reporting deadlines

R7M for due diligence failures + R3M for monitoring delays.

These institutions possessed substantial resources and professional compliance teams, yet faced significant penalties. The regulatory environment has evolved from advisory to enforcement-focused, with sophisticated oversight mechanisms detecting compliance gaps regardless of institutional profile.

ROI Analysis: The average compliance implementation investment represents approximately 2-5% of these penalty amounts, while providing ongoing operational and reputational benefits that far exceed initial costs.

Most law firms, property practitioners, and financial service providers believe they're compliant… until the Financial Intelligence Centre comes knocking.

The truth is:

Templates and DIY risk management plans are often not legally sufficient.

Staff rarely follow procedures consistently.

Gaps go unnoticed until they trigger penalties, audits, or reputational harm.

The cost?

Heavy fines, loss of client trust, even deregistration.

Imagine Compliance Made Simple — While You Focus on Clients

Compliance doesn’t have to be complicated or time-consuming. With the right systems in place, your organisation can stay fully FICA-compliant while you focus on what matters most — serving your clients.

Picture this:

No more worrying if your documents are up to standard.

Staff properly trained to handle compliance.

Confidence knowing you've covered your basis.

Peace of mind that you're protecting your institutions reputation.

True compliance also:

Builds client trust.

Makes your firm more attractive to banks, investors, and partners.

Gives you a competitive edge in a crowded market.

The FICA Friendly Way: Stress-Free Compliance for Accountable Institutions

FICA compliance doesn’t have to be overwhelming. The FICA Friendly Way™ helps institutions identify risks, close gaps, and stay audit-ready — all in a simple, structured tailored process as per FICA requirements.

Step 1: Check Your Compliance Gaps

Comlete a simple FICA self-audit—just 2 minutes to see whether your firm is secure or exposed.

Why this matters: This isn’t just a scorecard, it reveals hidden compliance gaps that could expose you to fines or reputational damage. Think of it as your early warning system.

Step 2: Close Compliance Gaps

Use the audit results to fix compliance weaknesses yourself — or partner with an experienced compliance team like FICA Friendly to get it done right the first time.

Why this matters: Unclosed gaps leave your firm exposed, and regulators won’t accept “we didn’t know” as an excuse.

Step 3: Stay FICA Audit-Ready

With regular training, updates, and expert guidance, you’ll always be prepared if the FIC comes knocking.

FIC says: Accountable institutions must “provide for risk management and compliance programmes, governance and training on combating money laundering and terrorist financing.” (FIC Guidelines)

DIY Compliance Can Be Costly.

Non-Compliance is Worse!

Trying to handle compliance on your own may seem like saving money— but hidden gaps can put your firm, your clients, and even you personally at serious risk.

Trying DIY compliance may feel like saving money, but:

Time Drain

It eats executive time better spent on clients.

Costly Mistakes

Mistakes can lead to penalties in the millions.

Personal Risk

You carry personal liability as a director or partner.

With FICA Friendly:

You spend less time worrying and less money fixing costly mistakes.

Inaction is even riskier. Regulators don't accept ignorance as an excuse.

Start by Discovering Your Compliance Score...

Before investing time or money into compliance, get clarity on where your institution really stands. In just 2 minutes, our self-audit gives you a snapshot of your FICA readiness — and points you toward the areas that need attention.

Free, instant results.

No obligation.

A clear path to compliance.

FAQ

Got questions?

The Financial Intelligence Centre Act (FIC Act) is South African legislation designed to combat money laundering, terrorist financing, and other financial crimes. If your business handles client funds, high-value transactions, or certain types of goods, you're legally required to comply. Non-compliance can result in fines exceeding R10 million, as seen with major institutions like ABSA Bank.

1. Legal practitioners

2. Business and trust service providers who assist clients to set up a business or manage trusts

3. Estate agents

4. Participants in South Africa’s financial markets

5. Casinos and businesses that engage in licensed gambling activities

6. Foreign exchange and credit providers dealing in currency transactions and lending

7. Financial services providers, including advisors and intermediaries

8. Businesses dealing in high-value goods and luxury items, particularly those making transactions of R100,000 or more

9. Crypto exchange providers

10. Participants in clearing systems and electronic systems, whether it’s processing credit card transactions, electronic transfers, or any kind of online payment

To download the comprehensive list click here.

The FIC conducts targeted audits, investigates suspicious transaction reports, responds to whistleblower reports, and performs sector-wide compliance reviews. They also monitor public records and can investigate based on client complaints or regulatory referrals.

Yes, if you handle client funds in trust accounts, facilitate property transactions, or deal with high-value matters, you're legally classified as an Accountable Institution under the FIC Act. Many successful firms discover this obligation only when facing penalties or audits.

The FIC has significantly increased enforcement activities. Recent penalties include R7.7 million against Kunene Ramapala Inc. (a law firm) and R3 million against Ninety One Fund Managers. The regulatory environment has shifted from warnings to substantial financial penalties.

Non-compliance with the Financial Intelligence Centre Act (FIC Act) can lead to significant administrative sanctions, including:

Financial Penalties: Fines up to R10 million for individuals and R50 million for legal entities.

Cautions and Reprimands: Formal warnings not to repeat the conduct that led to non-compliance.

Directives for Remedial Action: Orders to take specific steps to address compliance deficiencies.

Restriction or Suspension of Business Activities: Limiting or halting certain operations until compliance is achieved.

The FIC and other supervisory bodies assess the nature, seriousness, and extent of non-compliance when determining appropriate sanctions. They also consider any mitigating factors and may refer matters for criminal investigation if warranted.

To avoid these consequences, it's crucial for accountable institutions to implement and maintain effective compliance measures, conduct regular self-assessments, and address any identified gaps promptly.

Yes. Directors, partners, and senior executives can face personal liability for compliance failures. The FIC can pursue individuals who were responsible for ensuring compliance but failed to implement adequate measures.

Key requirements include: registering with the FIC, developing a Risk Management and Compliance Programme (RMCP), conducting customer due diligence, verifying beneficial ownership, screening clients against sanctions lists, filing regulatory reports, and providing staff training.

Templates or DIY checklists may seem convenient, but the FIC Act requires compliance measures to be risk-based and specific to your business. A “one-size-fits-all” approach often leaves gaps that regulators can penalize. Your RMCP and processes must reflect your actual services, clients, and risks.

Your RMCP should be reviewed atleast annually and updated whenever there are significant changes to your business, regulatory requirements, or risk environment. The FIC expects your programme to evolve with your business and the regulatory landscape.

While possible, compliance requires specialized knowledge of FIC requirements, risk assessment methodologies, and regulatory reporting. Most firms find that expert guidance ensures proper implementation while freeing up staff to focus on revenue-generating activities.

Partial compliance can be worse than no compliance, as it suggests awareness of obligations but failure to meet them. The FIC expects complete, properly implemented programmes. Half-measures won't protect you during an audit.

Properly implemented compliance actually strengthens client relationships by demonstrating professionalism and protecting both parties from financial crime risks. Banks and corporate clients increasingly prefer working with compliant institutions.

Frame it as protecting both your firm and your clients from financial crime risks. Most affluent clients appreciate working with institutions that take regulatory compliance seriously, as it reflects operational sophistication and reduces their own reputational risks.

A proper compliance assessment can be completed within days. The 2-minute self-audit provides immediate insights into potential gaps, while a comprehensive assessment typically takes 1-2 weeks depending on your firm's complexity.

Gaps are common and fixable. The key is addressing them promptly and systematically. With proper guidance, most firms can achieve full compliance within 4-8 weeks, depending on the extent of gaps and complexity of operations.

Reference List:

Financial Intelligence Centre Act, 38 of 2001

Source for: Legal definition of Accountable Institutions, compliance obligations, registration requirements

Financial Intelligence Centre Official Website

Main website: https://www.fic.gov.za/

About FIC: https://www.fic.gov.za/about/

Source for: FIC mandate, definition of financial intelligence unit, compliance oversight role

Legal Profession Guidance

Legal sector compliance: https://www.fic.gov.za/legal-sector/

Source for: Law firm specific obligations, trust account requirements

Property Sector Guidance

Property sector compliance: https://www.fic.gov.za/property-sector/

Source for: Estate agent and property practitioner requirements

Financial Services Guidance

Financial services compliance: https://www.fic.gov.za/financial-services/

Source for: FSP obligations, investment manager requirements

Banking Association Resources

Source for: Financial institution requirements, banking sector compliance

FIC Guidance Notes (Available on FIC website)

Guidance Note 1: General guidance on the FIC Act

Guidance Note 2: Customer identification and verification procedures

Guidance Note 3: Suspicious transaction reporting

Guidance Note 7A: Risk Management and Compliance Programme requirements

Available at: https://www.fic.gov.za/guidance-notes/

Source for: Specific compliance requirements, RMCP development, customer due diligence procedures

FATF Standards

Financial Action Task Force recommendations

Referenced at: https://www.fic.gov.za/international-cooperation/

Source for: International compliance standards, best practices

FIC Compliance Supervision

Supervision information: https://www.fic.gov.za/supervision/

Source for: Supervision procedures, audit processes, compliance expectations

FIC YouTube Channel

Channel: Financial Intelligence Centre South Africa https://www.youtube.com/@FinancialIntelligenceCentre

Video explanations of compliance requirements and obligations

Source for: Educational content referenced in landing page explainer video

Have a questions?

We're here to help!

+27728815095

info@ficafriendly.co.za

Boksburg, Gauteng.

Copyright © 2025 FICA FRIENDLY. All Rights Reserved.

Which email address should we send your obligation free Fica self-audit?

We HATE spam. Your email address is 100% secure